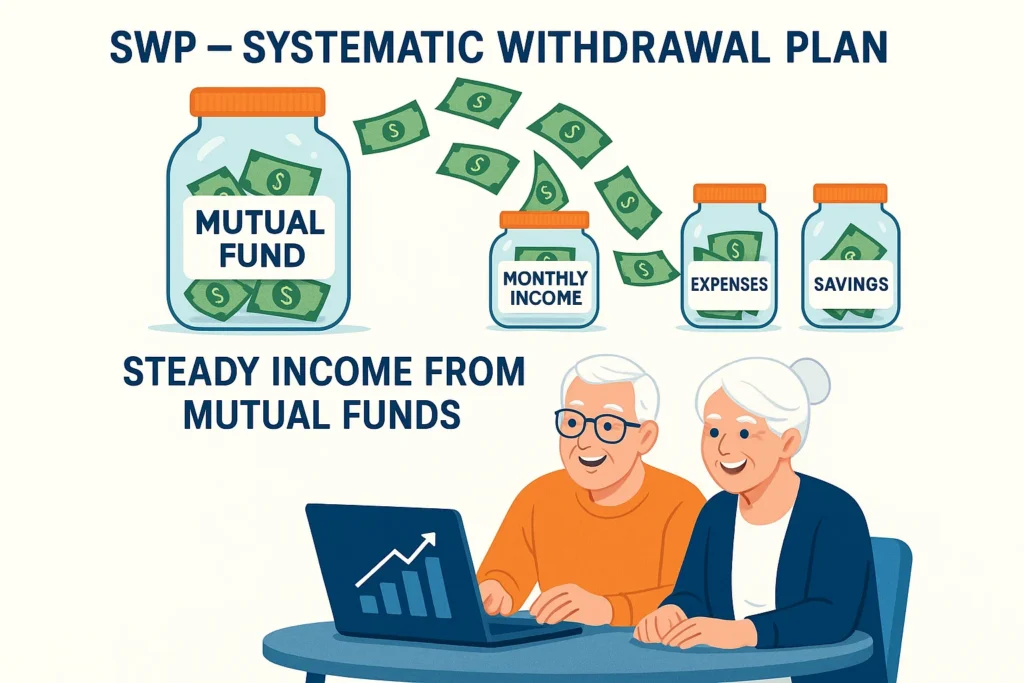

Introduction- Systematic Withdrawal Plan

Imagine this: you’ve worked for 30–40 years, saved diligently, and finally built a sizeable investment portfolio. Retirement begins, but a new question arises—how do I turn this lump sum into a reliable monthly income?

This is where SWP (Systematic Withdrawal Plan) comes into play.

Think of SWP as your very own “do-it-yourself pension.” You invest in mutual funds, and instead of withdrawing the entire amount or depending on unpredictable dividends, you set up a structured plan where money flows into your bank account every month. Simple, flexible, and surprisingly efficient.

In this SWP Complete Guide, we’ll walk through everything you need to know:

- How SWP really works in day-to-day life.

- Real calculation examples (with numbers and tables).

- Benefits and reasons why people choose SWP over other income options.

- Risks, limitations, and how to avoid mistakes.

- Practical strategies to make SWP sustainable for the long term.

- Real-life case studies to see how retirees actually use SWP.

Let’s dive in.

What is SWP(Systematic Withdrawal Plan)?

A Systematic Withdrawal Plan (SWP) is a facility offered by mutual funds that allows investors to withdraw a fixed amount of money at regular intervals. While SIP is all about putting money into mutual funds, SWP is about taking it out—gradually, and on your terms.

Here’s the beauty: when you opt for SWP, you don’t liquidate your investment in one go. Instead, the fund redeems a few units every month (or quarter, depending on the frequency you choose). The remaining units continue to stay invested and keep growing with market returns.

So, SWP helps you enjoy the best of both worlds: steady cash flow and capital growth.

How Does Systematic Withdrawal Plan Work?

Let’s break it down step by step, but instead of throwing theory, let’s make this relatable.

Say you invest ₹10,00,000 in a balanced mutual fund. You decide you’d like to receive ₹10,000 every month as a supplement to your retirement income.

Here’s what happens:

- Every month, the fund redeems enough units to give you ₹10,000.

- If the fund’s NAV is ₹50, the fund will redeem 200 units (10,000 ÷ 50).

- Next month, if NAV rises to ₹52, fewer units are redeemed (192.3 units).

- If NAV falls to ₹48, more units are redeemed (208.3 units).

This continues until you stop the plan or the corpus runs out.

Notice how your balance stays invested in the market and continues to generate returns. That’s the magic of SWP: you withdraw without killing the growth potential.

A Real Calculation Example of Systematic Withdrawal Plan

Numbers speak louder than concepts, so let’s see SWP in action.

Suppose:

- Initial investment: ₹10,00,000

- Annual expected return: 10%

- SWP amount: ₹10,000 per month

Here’s a simplified 3-year snapshot:

| Year | Opening Balance | Withdrawal (₹) | Growth @10% (₹) | Closing Balance |

|---|---|---|---|---|

| 1 | 10,00,000 | 1,20,000 | 88,000 | 9,68,000 |

| 2 | 9,68,000 | 1,20,000 | 84,800 | 9,32,800 |

| 3 | 9,32,800 | 1,20,000 | 80,800 | 8,93,600 |

After 3 years, you’ve already enjoyed ₹3,60,000 in withdrawals and still have ₹8,93,600 invested. That’s the balance between income and growth.

Now compare this with keeping money idle in a savings account or withdrawing everything upfront. You’d either lose out on growth or risk overspending. SWP solves both.

Check Your Monthly Withdrawal with SWP Calculator

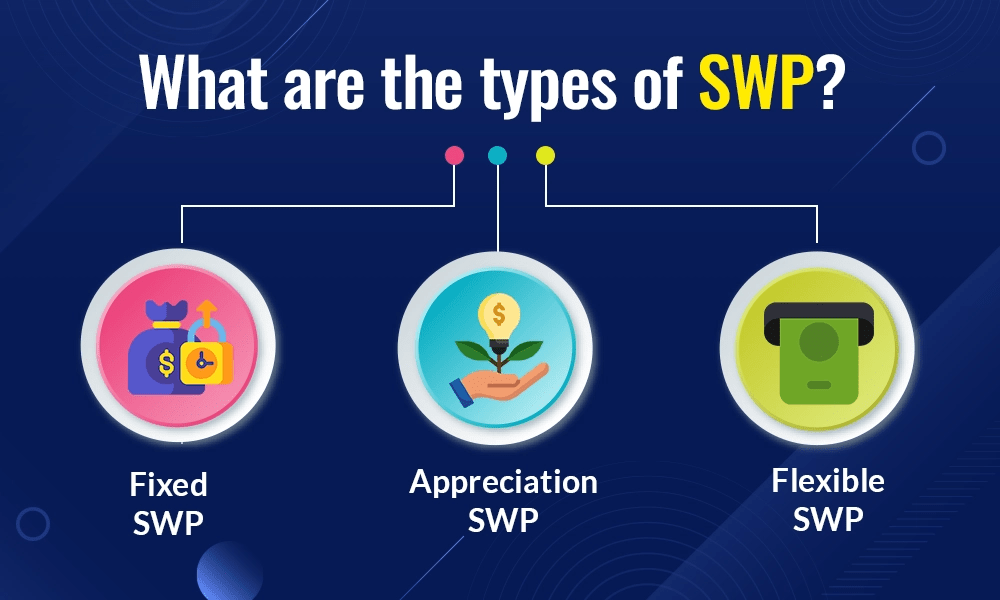

Types of SWP- A Complete Guide

While most people think of Systematic Withdrawal Plan as “fixed monthly income,” there are actually different types:

- Fixed SWP – You receive a fixed sum every month, e.g., ₹10,000. This is the most common option retirees choose.

- Appreciation SWP – Instead of withdrawing a fixed sum, you withdraw only the gains your investment has made. The original capital stays intact.

- Custom SWP – You decide irregular withdrawal amounts depending on your needs, e.g., more during festival seasons, less otherwise.

Each type has its place. Fixed Systematic Withdrawal Plan is predictable, Appreciation SWP preserves capital, and Custom SWP offers flexibility.

Benefits of Systematic Withdrawal Plan

Why is Systematic Withdrawal Plan becoming the go-to choice for so many investors, especially retirees? Let’s explore.

1. Regular Income Stream

With SWP, you can literally create your own pension. Every month, the same predictable amount arrives in your bank account—just like a salary.

2. Flexibility

Unlike annuities or fixed deposits, you’re not locked in. You can increase or decrease withdrawals, pause them, or even stop completely. This flexibility gives you control.

3. Capital Growth

Since only part of your investment is withdrawn, the rest stays invested and compounds. Over years, this can significantly extend the life of your portfolio.

4. Control Over Money

You decide how much to withdraw and when. No fund house or bank dictates terms.

5. Psychological Comfort

There’s a psychological advantage to seeing money flow in every month rather than worrying about managing a large lump sum.

Systematic Withdrawal Plan vs Other Options

It’s easier to understand Systematic Withdrawal Plan when we compare it with alternatives.

| Feature | SWP | SIP | Fixed Deposit | Dividend Payout | Annuity |

|---|---|---|---|---|---|

| Purpose | Withdraw money | Invest money | Earn fixed interest | Get profit share | Lifelong income |

| Flexibility | High | High | Low (penalty on breaking) | Low | Very low |

| Growth Potential | Moderate to high | High | Low | Low | None (locked) |

| Predictability | High | N/A | High | Medium | High |

| Control | Full | Full | Partial | None | None |

Clearly, SWP offers the rare combination of income + flexibility + growth.

Who Should Use Systematic Withdrawal Plan?

Not everyone needs an SWP. But for some, it’s a financial lifesaver.

- Retirees – SWP provides a steady monthly pension without depending entirely on children or irregular income sources.

- Business Owners – For those whose income fluctuates, SWP offers stability.

- Investors With Lump Sums – If you’ve received a bonus, inheritance, or sold property, SWP lets you convert that lump sum into manageable cash flow.

- Parents Planning for Kids’ Expenses – Education costs, marriage, or other big goals can be funded gradually with SWP.

Risks and Limitations of Systematic Withdrawal Plan

Of course, nothing in finance is risk-free. SWP has a few caveats you must keep in mind.

First, market fluctuations can impact your fund’s NAV. If markets fall sharply, more units get redeemed to pay your withdrawal, which can erode capital faster.

Second, if you withdraw too aggressively—say, 10% of your corpus every year—the fund will run dry sooner than later. SWP works best when withdrawals are sustainable (generally 4–6% annually).

Lastly, there is always the chance of underestimating expenses. While SWP is flexible, withdrawing too much too soon can undo years of careful planning.

Best Practices for Systematic Withdrawal Plan

So, how do you make Systematic Withdrawal Plan truly work for you? A few time-tested practices can help.

One, select the right fund category. Debt funds or hybrid funds are often safer choices for Systematic Withdrawal Plan compared to highly volatile small-cap equity funds.

Two, decide on a sustainable withdrawal rate. Many financial planners recommend the “4% rule”, meaning you withdraw only 4% of your corpus annually to ensure longevity.

Three, review your Systematic Withdrawal Plan annually. Just like you’d review your job or business income, revisit your withdrawal rate and fund performance once a year.

Four, diversify. Instead of putting all your corpus into one fund, spread across debt, hybrid, and large-cap funds. This cushions you against volatility.

A Real-Life Case Study

Let’s look at a retiree example to see how Systematic Withdrawal Plan plays out in real life.

Mr. Sharma, aged 60, retires with a corpus of ₹50 lakh. He wants a comfortable monthly income without eating into all his savings immediately. He chooses a conservative balanced fund and sets up an SWP of ₹40,000 per month.

Here’s a simplified 10-year projection (assuming 8% annual growth):

| Year | Corpus at Start | Withdrawal (₹40,000 x 12) | Growth (8%) | Corpus at End |

|---|---|---|---|---|

| 1 | 50,00,000 | 4,80,000 | 3,61,600 | 48,81,600 |

| 5 | 46,00,000 | 4,80,000 | 3,36,000 | 44,56,000 |

| 10 | 42,00,000 | 4,80,000 | 3,02,400 | 40,22,400 |

After a decade, Mr. Sharma has withdrawn nearly ₹48 lakh in income and still retains a corpus of over ₹40 lakh. That’s the dual power of SWP: regular cash flow + preserved capital.

The Psychological Side of SWP

Finance isn’t just about numbers; it’s about peace of mind. For many retirees, having money flow in every month reduces anxiety. It creates the sense of a “paycheck,” something they’ve been used to all their working life.

Contrast this with depending on children for money, or worrying about spending from a lump sum. SWP brings independence, dignity, and structure.

Building an SWP Strategy

If you’re considering setting up an Systematic Withdrawal Plan, here’s how to approach it.

- Assess Your Needs – Calculate monthly expenses. This helps you decide the withdrawal amount.

- Identify the Corpus – Figure out how much you can set aside for SWP without touching emergency funds.

- Pick Suitable Funds – For retirees, conservative hybrid or debt funds are ideal. For younger investors, equity SWPs may work.

- Set Withdrawal Frequency – Monthly is most common, but quarterly or annual is also possible.

- Monitor and Adjust – Review yearly and tweak if needed.

Remember: the aim is not just income, but sustainable income.

Conclusion

So that’s the SWP Complete Guide. We’ve walked through how it works, seen real calculations, explored benefits, compared it with alternatives, and even looked at real-life examples.

SWP is more than just a withdrawal facility—it’s a philosophy of managing wealth. It lets you enjoy life’s moments today while keeping your financial foundation intact for tomorrow.

If done wisely, Systematic Withdrawal Plan can provide retirees with dignity, business owners with stability, and families with flexibility. It transforms an investment corpus into a living, breathing income machine.

And perhaps the most beautiful part? It gives you the freedom to live life on your own terms, with steady cash flow and peace of mind.

FAQs for Systematic Withdrawal Plan (SWP)

1. What is a Systematic Withdrawal Plan (SWP)?

A Systematic Withdrawal Plan (SWP) allows you to withdraw a fixed amount from your mutual fund investment at regular intervals.

2. How does SWP work?

You invest a lump sum in a mutual fund, and then SWP redeems units periodically to give you fixed payouts.

3. Who should invest in SWP?

SWP is ideal for retirees, salaried individuals seeking regular cash flow, or anyone who wants steady income from investments.

4. What is the minimum amount for SWP?

Most mutual funds allow SWPs starting from ₹500–₹1,000 per month, though limits vary by AMC.

5. Can I stop or change my SWP?

Yes. You can pause, modify, or stop an SWP anytime without penalty.

6. What is the difference between SWP and SIP?

SIP helps you invest regularly, while SWP helps you withdraw regularly from an existing investment.

7. Is SWP better than FD for income?

SWP offers market-linked returns and flexibility, while FDs give fixed returns. SWP can be more tax-efficient and inflation-beating in the long run.

8. Can I start SWP immediately after investing?

Yes, many mutual funds allow you to start an SWP right after lump sum investment. Some may have a short lock-in period.

9. What happens if the fund value reduces?

If withdrawals exceed returns, your invested capital may reduce over time. Choosing the right fund and withdrawal rate is crucial.

10. Can NRIs use SWP?

Yes, NRIs can use SWP in mutual funds, subject to specific RBI and fund house rules.

Related Articles:

How to Transfer Shares to Family from One Demat to Another (2025 Guide)

How to Transfer Shares Between Demat Accounts Online: A Complete Guide

What Happens to Your Shares and Mutual Fund After Death? Transmission Process Explained

More Articles

Best Stock Broker in India: How to Choose Best Broker in 2025

The 15-15-15 Rule: Why the ₹1 Crore SIP Dream Needs a Reality Check

Gold vs Silver vs Sensex: Who Made You Richer?