Vikran Engineering IPO

The Vikran Engineering IPO is one of the most anticipated public issues in August 2025, hitting the markets with a size of ₹772 crore. The issue is a mix of a fresh issue worth ₹721 crore and an offer for sale (OFS) of ₹51 crore, signaling both fundraising for business expansion and partial exit for existing stakeholders.

With its diversified business in power transmission, water infrastructure, railways, and solar EPC, Vikran Engineering Ltd. has carved a strong niche as a fast-growing Engineering, Procurement, and Construction (EPC) company in India. The IPO opens for subscription on August 26, 2025, and closes on August 29, 2025, with listing expected on September 3, 2025, on both BSE and NSE.

This IPO comes at a time when India is aggressively expanding its infrastructure backbone, making Vikran Engineering a company to watch closely.

Vikran Engineering IPO Details

IPO Snapshot

| Particulars | Details |

|---|---|

| IPO Size | ₹772.00 crore |

| Fresh Issue | 7.43 crore shares (₹721.00 crore) |

| Offer for Sale | 0.53 crore shares (₹51.00 crore) |

| Price Band | ₹92 – ₹97 per share |

| Face Value | ₹1 per share |

| Lot Size | 148 shares |

| Minimum Retail Investment | ₹13,616 |

| Issue Type | Book Building Issue |

| Listing At | BSE, NSE |

| Pre-Issue Shares | 18,35,81,130 |

| Post-Issue Shares | 25,79,11,026 |

| Market Cap at Upper Band | ₹2,501.74 crore |

| Book Running Lead Manager | Pantomath Capital Advisors Pvt. Ltd. |

| Registrar | Bigshare Services Pvt. Ltd. |

Important Dates (Tentative)

| Event | Date |

|---|---|

| IPO Open Date | August 26, 2025 (Tuesday) |

| IPO Close Date | August 29, 2025 (Friday) |

| Basis of Allotment | September 1, 2025 (Monday) |

| Refunds Initiation | September 2, 2025 (Tuesday) |

| Credit of Shares | September 2, 2025 (Tuesday) |

| Listing Date | September 3, 2025 (Wednesday) |

| Cut-off Time for UPI Mandate | August 29, 2025, 5 PM |

Objects of the Issue

The company intends to utilize the net proceeds from the Vikran Engineering IPO for the following purposes:

- Funding working capital requirements – ₹541.00 crore

- General corporate purposes

Company Overview & Business Model – Vikran Engineering Ltd.

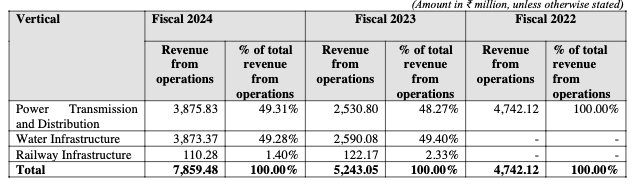

Incorporated in 2008, Vikran Engineering Ltd. has evolved into one of India’s fastest-growing Engineering, Procurement, and Construction (EPC) companies, offering turnkey solutions that cover design, supply, installation, testing, and commissioning. Its diversified portfolio is spread across power transmission & distribution, water infrastructure, railways, and solar EPC, with the first two contributing the lion’s share of revenues. In FY24, both power and water verticals accounted for about 49% each, while railways and solar made up the rest.

Power Transmission & Distribution

The power segment is the backbone of the company’s business. Vikran Engineering undertakes projects ranging from high-voltage transmission lines (up to 765 kV) to extra-high voltage substations (up to 400 kV) and large-scale distribution networks. It has executed notable assignments such as the 765 kV AIS bays in Raipur, the 400 kV Bina substation, and the 500 MVA transformer installation at Muzaffarpur in Bihar. The company has also diversified into smart metering, having completed more than 30,000 connections under this vertical.

Water Infrastructure

The water vertical mirrors the scale of power in terms of revenue contribution. Here, the company executes underground and surface water distribution networks, overhead tanks, and rainwater harvesting systems. Growth in this area is driven by large public spending under schemes such as Jal Jeevan Mission, AMRUT, Swachh Bharat Mission, and the National Mission for Clean Ganga. With these government programs expected to nearly double sectoral investments between FY25 and FY29, Vikran Engineering has strong visibility in this space.

Railway and Solar Projects

Though relatively smaller contributors, railways and solar EPC add important diversification. The company has worked on railway electrification projects, including 132 kV traction substations, underground EHV cabling, and OHE (25 kV) electrification systems, while its solar EPC work includes ground-mounted projects and smart metering initiatives.

Here is the details of contribution to revenue from operations as per DRHP:

Order Book & Clientele

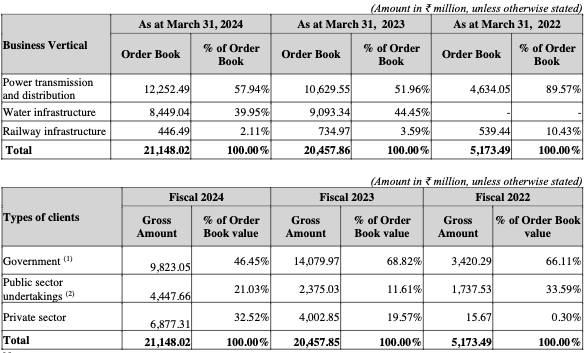

The company’s order book growth has been impressive, rising from just ₹5,173 million in FY22 to ₹21,148 million in FY24, reflecting both scale and diversification. As of August 2024, Vikran Engineering was executing 34 ongoing projects across 17 states, supported by a strong history of 44 completed projects across 11 states.

Here is the Snapshot of the company’s Order book as per DRHP:

Its client base is equally diversified, spanning government bodies, PSUs, and private players. Major clients include NTPC, Power Grid, Transmission Corporation of Telangana, and multiple state water and sanitation missions. In FY24, government contracts accounted for nearly 46% of the order book, with PSUs at 21% and private sector clients contributing over 32%, indicating reduced dependence on a single customer group.

Competitive Strengths

What makes Vikran Engineering stand out is its ability to deliver projects within or ahead of contractual timelines, supported by:

- In-house design and engineering capabilities for efficient execution.

- A pan-India presence with 195 project sites ensuring local support.

- A network of over 3,500 suppliers, which minimizes supply chain risks and ensures material availability.

This operational excellence has translated into strong financial growth. Between FY22 and FY24, PAT grew at a CAGR of 236.9%, while EBITDA expanded at 130% CAGR. Return ratios such as ROE and ROCE are among the best in the EPC peer group, according to CRISIL.

Industry Tailwinds

The company also benefits from structural growth drivers in India’s infrastructure sector. Transmission line capacity has been steadily rising, while the water sector alone is expected to see investments of ₹9.9 trillion by FY29, more than double the ₹4.4 trillion deployed during FY19–24. These long-term drivers ensure a sustained pipeline of opportunities for players like Vikran Engineering.

In summary, Vikran Engineering Ltd. is more than just an EPC contractor. Its strength lies in a balanced business model, strong execution track record, marquee client base, and robust financial performance, making it well-positioned to capture India’s next wave of infrastructure growth.

Vikran Engineering IPO – Financial Performance

Vikran Engineering Ltd. has demonstrated a steady upward trajectory in its financials over the past three years, reflecting strong project execution capabilities and a diversified order book. Between FY24 and FY25, revenue grew by 17%, while profit after tax (PAT) rose by 4%, underlining the company’s ability to sustain growth even in a competitive EPC environment.

Financial Summary (₹ Crore)

| Period Ended | 31 Mar 2025 | 31 Mar 2024 | 31 Mar 2023 |

|---|---|---|---|

| Assets | 1,354.68 | 959.79 | 712.47 |

| Total Income | 922.36 | 791.44 | 529.18 |

| EBITDA | 160.24 | 133.30 | 79.71 |

| PAT | 77.82 | 74.83 | 42.84 |

| Net Worth | 467.87 | 291.28 | 131.14 |

| Reserves & Surplus | 449.52 | 290.95 | 130.85 |

| Borrowings | 272.94 | 183.39 | 154.92 |

Key Financial Highlights

- Consistent Growth: Total income almost doubled from ₹529.18 crore in FY23 to ₹922.36 crore in FY25, showing a CAGR of ~32%.

- Profitability: PAT increased from ₹42.84 crore in FY23 to ₹77.82 crore in FY25, though FY24–25 growth was modest at 4%.

- Operational Efficiency: EBITDA more than doubled in two years, reaching ₹160.24 crore in FY25, supported by execution efficiency and cost management.

- Strengthened Balance Sheet: Net worth rose over 3.5x in just two years, from ₹131.14 crore in FY23 to ₹467.87 crore in FY25, improving financial resilience.

Ratios & Margins

The company’s financial ratios highlight operational strength and efficient capital usage:

- ROE: 16.63% – showcasing healthy shareholder returns.

- ROCE: 23.34% – among the stronger returns in the EPC industry.

- PAT Margin: 8.44% – demonstrating steady profitability despite sectoral challenges.

- EBITDA Margin: 17.50% – indicating operational efficiency.

- Debt/Equity Ratio: 0.58 – a moderate leverage position, suggesting room for debt-funded expansion without significant risk.

- RoNW: 16.63% – consistent with sector leaders.

Valuation & Peer Comparison

Valuation Metrics

At the upper end of the price band, the Vikran Engineering IPO is valued at a market capitalization of ₹2,501.74 crore. Based on FY25 earnings, the stock is priced at:

- P/E Ratio: 22.88x (Pre-IPO) and 32.15x (Post-IPO, diluted)

- Price-to-Book Value (P/BV): 3.81x

This valuation indicates that the company is entering the market at a premium compared to some mid-sized EPC peers, although it sits below the high multiples of niche players like Bajel Projects.

Peer Comparison

Below is a peer set comparison of Vikran Engineering Ltd. with other listed infrastructure and EPC players (as of March 31, 2025):

| Company | EPS (Basic) | NAV (₹/share) | P/E (x) | RoNW (%) | P/BV Ratio |

|---|---|---|---|---|---|

| Vikran Engineering Ltd. | 4.35 | 25.49 | 22.88 – 32.15 | 16.63 | 3.81 |

| Bajel Projects Ltd. | 1.34 | 57.63 | 158.75 | 2.32 | 3.72 |

| Kalpataru Projects Intl. | 35.53 | 378.80 | 34.68 | 8.77 | 3.26 |

| Techno Electric & Engg. | 37.19 | 321.55 | 40.17 | 11.31 | 4.65 |

| SPML Infra Ltd. | 7.61 | 107.43 | 36.79 | 6.22 | 2.61 |

| KEC International Ltd. | 21.80 | 200.88 | 35.71 | 10.67 | 3.89 |

| Transrail Lighting Ltd. | 25.72 | 140.11 | 30.73 | 17.36 | 5.64 |

Compared to peers:

- Earnings & Growth: Vikran Engineering’s EPS is modest compared to larger players like Kalpataru, KEC, and Techno Electric, but the 16.63% RoNW reflects efficient capital usage, ahead of many established EPC players.

- Valuation: Its P/E range (22.88x–32.15x) positions it more expensive than SPML Infra and KEC International but cheaper than Bajel Projects (158x).

- P/BV at 3.81x is aligned with industry averages (3–4x) but slightly lower than high-quality niche players like Transrail (5.64x).

- Takeaway: The IPO looks reasonably priced relative to mid-cap EPC peers, though investors are paying a premium for its strong RoNW and double-digit margins.

Strengths & Risks of Vikran Engineering IPO

| Strengths | Risks / Concerns |

|---|---|

| Robust Financial Growth – Revenue grew 17% and PAT rose 4% YoY (FY25 vs FY24). | High Valuation – Post-IPO P/E at ~32x, higher than some established EPC peers. |

| Healthy Margins – EBITDA margin at 17.5% and PAT margin at 8.4%, showcasing operational efficiency. | Debt Burden – Debt/Equity at 0.58; borrowings increased to ₹272.94 Cr (FY25), which could impact future cash flows. |

| Strong Return Ratios – RoNW at 16.63% and RoCE at 23.34%, superior to several listed peers. | Competitive Industry – Faces intense competition from established EPC players like Kalpataru, KEC, and Techno Electric. |

| Diversified Project Portfolio – Presence in infrastructure, power transmission, and engineering services reduces sectoral dependency. | Cyclicality in Orders – EPC business is directly linked to government spending and economic cycles. |

| Experienced Management – Backed by seasoned leadership with industry expertise. | Execution Risks – Project delays, cost overruns, and regulatory challenges could affect profitability. |

Vikran Engineering IPO GMP (Grey Market Premium)

The grey market premium (GMP) is often considered an early indicator of how the market perceives an IPO before its official listing. For the Vikran Engineering IPO, the GMP has shown an upward trend, suggesting positive investor sentiment.

Vikran Engineering IPO GMP Trend

| Date | IPO Price | GMP | Sub2 Sauda Rate | Estimated Listing Price | Estimated Profit* | Movement |

|---|---|---|---|---|---|---|

| 19 Aug 2025 | ₹97.00 | ₹12 | 1300/18200 | ₹109 (12.37%) | ₹1,776 | GMP Up |

*Estimated profit is based on the lot size and current GMP levels.

What this means for investors

With the GMP at ₹12, the estimated listing price comes to around ₹109 per share, representing a 12.37% listing gain over the issue price of ₹97. The upward movement in GMP indicates healthy demand in the unofficial market, but as always, GMP is speculative and should not be the sole basis for investment decisions.

Conclusion – View on Vikran Engineering IPO

The Vikran Engineering IPO presents an interesting mix of growth visibility and valuation challenges. On one hand, the company has delivered a 17% revenue growth and steady improvement in profitability, supported by strong margins (EBITDA margin at 17.5%). Its financial position is decent with a debt-to-equity ratio of 0.58, suggesting manageable leverage.

However, valuation is where caution arises. At a post-IPO P/E of 32.15x and P/BV of 3.81x, the issue looks slightly expensive compared to larger established peers in the EPC and infrastructure space. Still, its RoNW of 16.63% and ROCE of 23.34% are attractive, showing efficient capital utilization. The GMP trend (+₹12) indicates positive listing interest, which could support short-term gains.

In short, the IPO suits investors with a balanced perspective — those seeking short-term listing benefits as well as long-term exposure to India’s growing infrastructure sector.

Short-Term Strategy

Given the healthy GMP and upbeat demand, investors can consider applying for listing gains. A potential 10–15% upside on listing looks achievable, though volatility around market sentiment should be factored in.

Long-Term Strategy

From a long-term perspective, Vikran Engineering’s growth visibility is backed by its expanding order book and efficient execution. While valuations are not cheap, the company’s high ROCE and strong operating margins justify a premium to some peers. Long-term investors can view this IPO as a structural play on India’s infrastructure push, provided they are comfortable with cyclical risks in the EPC sector.

Allotment Strategy

Given the oversubscription potential and positive GMP, retail investors may consider applying in multiple applications (family accounts) to improve chances of allotment. Conservative investors, however, should weigh valuations before committing heavily.

Final Takeaway: Vikran Engineering IPO offers a sweet mix of growth and momentum — attractive for short-term players, promising for long-term believers.

FAQs on Vikran Engineering IPO

Q1. What is the Vikran Engineering IPO price band?

The IPO price is fixed at ₹97 per share.

Q2. What is the Vikran Engineering IPO lot size?

Investors can bid for a minimum of 150 shares per lot.

Q3. What are the IPO opening and closing dates?

The IPO opens on 19 August 2025 and closes on 21 August 2025.

Q4. What is the market capitalization of Vikran Engineering post-IPO?

The post-issue market cap is around ₹2,501.74 crore.

Q5. How has the company performed financially in FY25?

In FY25, revenue grew 17% and PAT rose 4% year-on-year.

Q6. What is the Vikran Engineering IPO GMP today?

As of 19 August 2025, GMP is around ₹12, indicating ~12% listing gains.

Q7. What is the P/E ratio of Vikran Engineering IPO?

The IPO is valued at a P/E of 32.15x (post-issue).

Q8. Is Vikran Engineering IPO good for listing gains?

Yes, based on GMP trends, a 10–15% listing gain looks possible.

Q9. How does Vikran Engineering compare with peers?

It trades at a premium compared to some peers but has stronger ROCE (23.34%) and margins.

Q10. Should I apply for Vikran Engineering IPO?

Investors can consider it for short-term gains and long-term growth exposure in infrastructure.

Related Articles

How to Analyze an IPO Before Investing: A Step-by-Step Guide

One Demat vs Multiple Demat – Which is Better for IPO Allotment?