Introduction

Think India’s retail growth is only about glitzy metro malls? Think again. The Patel Retail IPO is bringing the spotlight to tier-III cities and bustling suburban markets.

Under the brand Patel’s R Mart, the company runs neighbourhood supermarkets that pack in everything — fresh groceries, FMCG, apparel, and even their own private labels. Customers walk in for pulses and spices but often leave with much more.

Opening on August 19, 2025, this ₹242.76 crore IPO is more than a capital raise. It’s a launchpad for faster expansion, stronger branding, and a bigger bite of India’s growing FMCG pie. Short-term traders, long-term investors — this one might have something for everyone.

In this blog, we’ll break down every detail — IPO specifics, financials, valuations, strengths, risks, and even strategies for allotment and listing gains — so you can decide if Patel Retail IPO deserves a place in your portfolio

Patel Retail IPO Details: Everything You Need to Know

The Patel Retail IPO is a book-building issue worth ₹242.76 crore. It’s a mix of:

- Fresh Issue: 0.85 crore shares, raising ₹217.21 crore

- Offer for Sale (OFS): 0.10 crore shares, raising ₹25.55 crore

IPO Details

| Particulars | Details |

|---|---|

| IPO Date | August 19, 2025 to August 21, 2025 |

| Listing Date | August 26, 2025 (Tentative) |

| Face Value | ₹10 per share |

| Price Band | ₹237 – ₹255 per share |

| Lot Size | 58 shares |

| Minimum Retail Investment | ₹13,746 |

| Issue Size | 95,20,000 shares (₹242.76 Cr) |

| Fresh Issue | 84,67,000 shares (₹215.91 Cr) |

| Offer for Sale | 10,02,000 shares (₹25.55 Cr) |

| Listing At | BSE, NSE |

| Book Running Lead Manager | Fedex Securities Pvt Ltd |

| Registrar | Bigshare Services Pvt Ltd |

| Employee Reservation | 51,000 shares at ₹20 discount |

IPO Timeline

| Event | Date |

|---|---|

| IPO Opens | August 19, 2025 |

| IPO Closes | August 21, 2025 |

| Allotment Finalisation | August 22, 2025 |

| Refund Initiation | August 25, 2025 |

| Shares Credit to Demat | August 25, 2025 |

| Listing Date | August 26, 2025 |

| UPI Mandate Cut-off | 5 PM, August 21, 2025 |

Patel Retail IPO Objectives

The company plans to use the net proceeds for:

- Repayment/Prepayment of certain borrowings – ₹59 crore

- Funding working capital – ₹115 crore

- General corporate purposes

About Patel Retail Ltd

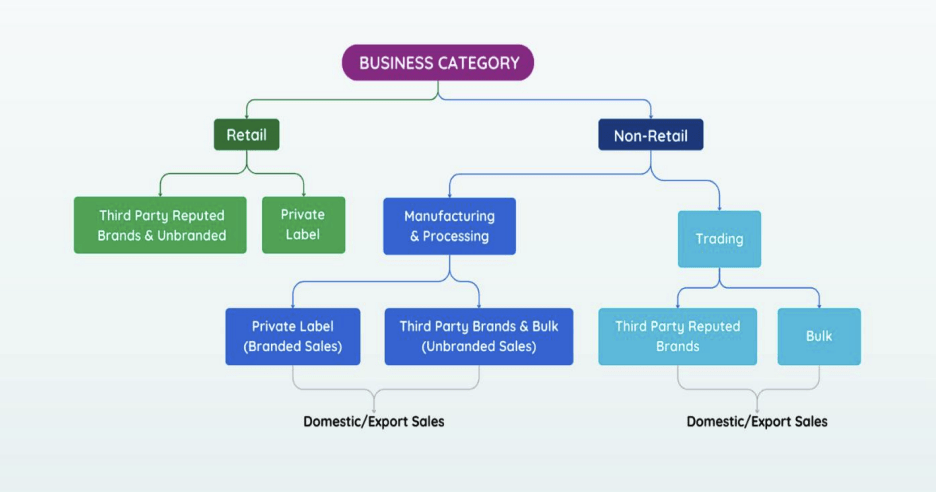

Patel Retail Ltd is not your typical retail chain chasing high-end malls in metros. Instead, it has carved a niche as a value retail supermarket chain operating primarily in tier-III cities and nearby suburban areas. The focus is clear — offer food, FMCG, general merchandise, and apparel for the entire family, at prices that keep customers coming back.

Founded in 2008, the company opened its first store in Ambernath, Maharashtra under the brand “Patel’s R Mart”. Fast forward to May 31, 2025, and the network has grown to 43 stores spread across the suburban areas of Thane and Raigad districts in Maharashtra, with a total retail business area of approximately 1,78,946 sq. ft.

Private Labels: Driving Margins and Brand Loyalty

To improve margins and build brand recognition, Patel Retail launched its own private label products, including:

- Patel Fresh – Pulses, ready-to-cook mixes, and instant food

- Indian Chaska – Spices, ghee, papad

- Blue Nation – Men’s wear

- Patel Essentials – Home improvement products

Products are sourced in bulk, processed, and packaged at the Ambernath facility (Facility 1) after stringent quality checks. Some items are also sourced from third-party vendors under Patel’s in-house brands.

Backward Integration and Manufacturing Strength

The company’s supply chain efficiency is backed by strategically located manufacturing facilities:

- Facility 1 (Ambernath, Maharashtra): Processing, quality checks, and packaging of private label grocery items.

- Facility 2 (Dudhai, Kutch, Gujarat): Processing of peanuts, coriander seeds, and cumin seeds.

- Facility 3 – Agri-Processing Cluster (Dudhai, Kutch, Gujarat): Spread over 15.925 acres, it houses five production units, a fruit pulp processing unit, a dry warehouse (3,040 MT), a cold storage facility (3,000 MT), and an in-house testing & research lab.

Facilities 2 and 3 together form the Kutch Facilities, while all three sites collectively are known as the Manufacturing Facilities.

Domestic & Global Footprint

Capitalising on its sourcing strength, Patel Retail has ventured into exports of staples, groceries, pulses, spices, and fruit pulps under the Patel Fresh and Indian Chaska brands — as well as private labels for clients. The company exports to 35+ countries, alongside domestic trading of FMCG goods, household items, kitchen appliances, and bulk agri commodities like rice, sugar, pulses, and edible oil.

With over 38 product categories and more than 10,000 SKUs, Patel Retail has built a product mix that caters to everyday needs while opening new revenue streams through manufacturing, exports, and bulk trading.

Patel Retail IPO Financials

Patel Retail Ltd has shown steady financial performance over the last three fiscal years, with consistent growth in profitability despite fluctuations in revenue. The company’s focus on private labels, efficient supply chain, and expansion in retail footprint have helped maintain healthy margins.

Restated Financial Information (₹ in Crores)

| Particulars | FY 2023 | FY 2024 | FY 2025 | CAGR (% FY23–FY25) |

|---|---|---|---|---|

| Assets | 303.12 | 333.02 | 382.86 | 12.3% |

| Total Income | 1,019.80 | 817.71 | 825.99 | -9.9% |

| EBITDA | 43.24 | 55.84 | 62.43 | 20.3% |

| Profit After Tax (PAT) | 16.38 | 22.53 | 25.28 | 24.1% |

| Net Worth | 71.87 | 94.40 | 134.57 | 37.1% |

| Total Borrowings | 182.81 | 185.75 | 180.54 | -0.6% |

Key Observations:

- Revenue dipped from FY23 to FY24 but recovered slightly in FY25.

- EBITDA and PAT have grown steadily, indicating better operational efficiency.

- Net worth has nearly doubled in two years, strengthening the balance sheet.

- Debt levels remain stable, reflecting controlled leverage.

Key Financial Ratios & KPIs (FY25)

| KPI | Value |

|---|---|

| Return on Equity (ROE) | 19.02% |

| Return on Capital Employed (ROCE) | 14.43% |

| Debt-to-Equity | 1.34 |

| Return on Net Worth (RoNW) | 19.02% |

| PAT Margin | 3.08% |

| EBITDA Margin | 7.61% |

| Price-to-Book Value (P/B) | 4.72 |

| Market Capitalisation | ₹851.71 Cr |

Takeaway for Investors:

While revenue growth has been modest, margin improvement and strong return ratios indicate that Patel Retail is moving towards a more profitable and sustainable growth path. The company’s private label focus and backward integration could further support margin expansion in the future.

Patel Retail IPO Valuation & Peer Comparison

IPO Valuation

At the upper price band, Patel Retail’s valuation works out to:

| Metric | Pre-IPO | Post-IPO |

|---|---|---|

| EPS (₹) | 10.16 | 7.57 |

| P/E (x) | 25.10 | 33.69 |

| Price-to-Book Value (P/BV) | — | 4.72 |

A post-IPO P/E of 33.69x puts Patel Retail in the mid-range compared to premium FMCG/retail peers like Avenue Supermarts, but higher than some smaller retail chains.

Peer Comparison

| Company | EPS (Basic) | NAV (₹) | P/E (x) | RoNW (%) | P/BV |

|---|---|---|---|---|---|

| Patel Retail | 10.30 | 54.08 | 33.69* | 19.02 | 4.72 |

| Vishal Mega Mart | 1.40 | 13.92 | 104.73 | 9.87 | 11.23 |

| Avenue Supermarts | 41.61 | 329.27 | 102.33 | 12.64 | 12.94 |

| Spencers Retail | -27.33 | -73.40 | — | -37.24 | -0.78 |

| Osia Hyper Retail | 1.46 | 23.85 | 8.73 | 4.97 | 0.52 |

| Aditya Consumer Marketing | -2.62 | 14.14 | — | -18.51 | 3.00 |

| Sheetal Universal | 8.12 | 38.27 | 15.58 | 21.44 | 3.32 |

| Kovilpatti Lakshmi Roller Flour Mills | 1.27 | 73.92 | 101.61 | 1.72 | 1.77 |

| KN Agri Resources | 14.76 | 140.60 | 17.01 | 10.50 | 1.79 |

| Madhusudhan Masala Ltd | 10.93 | 64.73 | 12.92 | 16.04 | 2.20 |

*Post-IPO P/E based on diluted EPS of ₹7.57.

Valuation Takeaway:

Patel Retail’s P/E multiple is lower than large-cap giants like Avenue Supermarts but significantly higher than smaller peers like Osia Hyper Retail or KN Agri Resources. Its P/BV ratio of 4.72 is moderate compared to Vishal Mega Mart’s 11.23, suggesting a fairer asset-based valuation. The key driver justifying the valuation will be consistent margin growth from private labels and expansion into high-potential tier-III markets.

Strengths & Risk Factors

| Strengths | Risk Factors |

|---|---|

| Strong retail network with presence across multiple locations, boosting market reach and brand visibility. | High dependence on consumer spending trends – slowdown in demand could impact revenues. |

| Consistent revenue growth supported by increasing footfall and product range expansion. | Intense competition from both organized and unorganized retail players, affecting margins. |

| Diversified product portfolio catering to various customer segments, reducing category-specific risks. | Thin operating margins typical in retail sector, making profitability sensitive to cost fluctuations. |

| Established supplier relationships ensuring steady inventory supply and competitive pricing. | High working capital requirements due to large inventory needs. |

| Potential for e-commerce expansion to tap into online retail growth. | Dependence on physical store operations – disruptions (like pandemics) can hurt sales. |

Patel Retail IPO GMP (Grey Market Premium)

GMP Trend

| GMP Date | IPO Price (₹) | GMP | Estimated Listing Price (₹) | Estimated Profit* |

|---|---|---|---|---|

| 11-08-2025 | 255.00 | ₹20 (No Change) | 275 (7.84%) | ₹1160 |

*Estimated profit is calculated based on the latest GMP and IPO price.

GMP Insight:

As of August 11, 2025, Patel Retail IPO is trading at ₹20 GMP, indicating 7.84% premium in the grey market. This suggests that market participants are currently neutral, possibly awaiting subscription data or broader market cues before making aggressive bets.

Conclusion

The Patel Retail IPO brings an interesting retail-sector play to the market with its growing revenue, strong store presence, and expansion potential. However, investors should also be aware of the risks—particularly the dependency on specific suppliers, seasonal demand fluctuations, and the competitive retail landscape. The IPO pricing appears reasonable given the company’s recent growth momentum, but sustained profitability will depend on its ability to execute expansion plans efficiently and manage operational costs.

Short-Term Strategy

Given the brand’s strong regional positioning and current IPO market sentiment, short-term traders may consider applying for listing gains. Retail-focused consumer companies often witness healthy demand during listing if market sentiment is bullish. Monitoring GMP (Grey Market Premium) and subscription figures during the IPO window will be key for deciding exit timing.

Long-Term Strategy

For long-term investors, the stock may offer growth potential if the company sustains its revenue trajectory, manages costs, and expands its footprint effectively. The rising organised retail penetration in India and consumer demand growth offer favorable tailwinds. However, given the competitive nature of retail, holding for the long term would require tracking quarterly performance closely.

Allotment Strategy

- Retail Investors: Apply in the retail category to maximise allotment probability; oversubscription is possible due to the brand’s growth story.

- HNI/NII Investors: Consider bidding in small HNI (S-HNI) category to enhance allotment chances if retail demand surges.

- Monitoring Tip: Watch subscription data on Day 2 and Day 3—if QIB participation is strong, the probability of a positive listing increases.

Patel Retail IPO — a growing regional retail brand aiming for a national footprint, but investors must weigh growth potential against valuation risks.

FAQs: Patel Retail IPO

What is the Patel Retail IPO issue size?

₹242.76 crore.

When does the Patel Retail IPO open and close?

Opens August 19, 2025 and closes August 21, 2025.

What is the Patel Retail IPO price band?

₹237 to ₹255 per share.

What is the lot size and minimum retail investment?

Lot size 58 shares; minimum retail investment ₹13,746 (58 × ₹237).

Is Patel Retail IPO a fresh issue or an OFS?

It’s a mix — Fresh Issue (84,67,000 shares) + Offer for Sale (10,02,000 shares).

On which exchanges will Patel Retail list and when?

Listing on BSE & NSE, tentative listing date August 26, 2025.

Who are the book running lead manager and registrar?

Fedex Securities Pvt Ltd (BRLM) and Bigshare Services Pvt Ltd (Registrar).

What is the reservation/allocation split?

Retail: ≥45% of net offer; NII: ≥25%; QIB: ≤30%; plus 51,000 shares reserved for employees.

What are the key FY25 financials / KPIs?

FY25 — Total Income: ₹825.99 Cr; PAT: ₹25.28 Cr; EBITDA: ₹62.43 Cr; ROE: 19.02%; P/B: 4.72.

What will the IPO proceeds be used for?

Repayment/prepayment of borrowings (₹59 Cr), working capital (₹115 Cr), and general corporate purposes.

Related Articles

How to Analyze an IPO Before Investing: A Step-by-Step Guide

One Demat vs Multiple Demat – Which is Better for IPO Allotment?