Anlon Healthcare IPO – Will It Be the Next Multibagger in Pharma?

The healthcare and pharmaceutical space in India has been buzzing with strong growth, fueled by rising medical needs, government push, and increasing global demand. Riding on this wave, Anlon Healthcare Ltd is coming up with its IPO, aiming to unlock new growth opportunities.

But the big question is – should investors subscribe to the Anlon Healthcare IPO, or wait on the sidelines? With its presence in pharma formulations and growing export demand, the company is pitching itself as a high-potential player in the sector.

In this blog, we’ll break down everything you need to know – IPO details, financial performance, valuations, peer comparison, GMP trend, and strategies – so you can make an informed decision before applying.

Anlon Healthcare IPO Details

Anlon Healthcare is coming with a 100% fresh issue to fund expansion, strengthen the balance sheet, and support working capital. It’s a book-built mainboard IPO that will list on both BSE & NSE.

IPO Snapshot

| Particulars | Details |

|---|---|

| Issue Type | Bookbuilding IPO (Mainboard) |

| Total Issue Size | ₹121.03 Cr |

| Fresh Issue | 1.33 Cr shares (₹121.03 Cr) |

| Offer for Sale (OFS) | NA (No OFS) |

| Price Band | ₹86 – ₹91 per share |

| Face Value | ₹10 per share |

| Lot Size | 164 shares |

| Minimum Retail Investment | ₹14,104 (@ ₹86) / ₹14,924 (@ ₹91) |

| sNII Benchmark | 14 lots = 2,296 shares ≈ ₹2,08,936 (@ ₹91) |

| bNII Benchmark | 68 lots = 11,152 shares ≈ ₹10,14,832 (@ ₹91) |

| Reservation | QIB ≥75%, NII ≥15%, Retail ≤10% (of Net Issue) |

| Listing | BSE, NSE |

| Pre-Issue Shares | 3,98,51,500 |

| Post-Issue Shares | 5,31,51,500 |

| Promoter Holding (Pre) | 70.26% |

| Promoter Holding (Post)** | ~52.7% (est., no OFS) |

| Book Running Lead Manager | Interactive Financial Services Ltd. |

| Registrar | Kfin Technologies Ltd. |

**Estimated post-issue holding assumes no change in promoter share count (fresh issue only).

Important Dates (Tentative)

| Event | Date |

|---|---|

| IPO Open Date | Tue, Aug 26, 2025 |

| IPO Close Date | Fri, Aug 29, 2025 |

| Basis of Allotment | Mon, Sep 1, 2025 |

| Initiation of Refunds | Tue, Sep 2, 2025 |

| Credit of Shares to Demat | Tue, Sep 2, 2025 |

| Listing Date | Wed, Sep 3, 2025 |

| UPI Mandate Cut-off | 5 PM on Aug 29, 2025 |

Objects of the Issue

- Funding capex for proposed expansion – ₹3,071.95 million

- Repayment/prepayment of certain secured borrowings – ₹500 million

- Funding working capital requirements – ₹4,315 million

- General corporate purposes

Amounts presented as provided in the filing. Allocation of net proceeds will follow the final RHP; total project outlays can be higher than IPO proceeds and may be funded through a mix of sources.

Company Overview & Business Model – Anlon Healthcare Ltd.

Anlon Healthcare is a chemical manufacturing company specializing in high-purity pharmaceutical intermediates (Pharma Intermediates) and active pharmaceutical ingredients (APIs), which serve as the backbone of the global healthcare and pharmaceutical industry. These products are critical raw materials for manufacturing Finished Dosage Formulations (FDFs) such as tablets, capsules, syrups, ointments, and are also widely used in nutraceuticals, personal care products, and veterinary medicines.

One of the company’s key strengths lies in manufacturing APIs that adhere to stringent international standards, including IP, BP, EP, JP, and USP pharmacopeia guidelines. In fact, Anlon Healthcare is one of the very few Indian manufacturers of loxoprofen sodium dihydrate, a widely prescribed anti-inflammatory and pain-relief drug used for conditions like rheumatoid arthritis, osteoarthritis, back pain, frozen shoulder, and post-surgery recovery.

In recent years, the company has also expanded into custom manufacturing services, catering to novel and complex chemical compounds. This business line is designed to meet specific client requirements, including achieving purity levels that exceed conventional industry benchmarks. Such capability highlights the company’s R&D-driven approach and domain expertise.

Regulatory Footprint

To strengthen its global presence, Anlon Healthcare has secured regulatory approvals for its APIs from leading international agencies. For example:

- ANVISA (Brazil), NMPA (China), and PMDA (Japan) have approved loxoprofen sodium dihydrate.

- The company has also filed 21 Drug Master Files (DMFs) with regulatory authorities across the EU, Russia, Japan, South Korea, Iran, Jordan, and Pakistan.

- Upcoming filings include Ketoprofen in the U.S. and Dexketoprofen Trometamol in Spain, Italy, Germany, and Slovenia.

Product Portfolio

The company currently has a robust portfolio of 142 products, covering Pharma Intermediates, APIs, Nutraceutical APIs, Personal Care Intermediates, and Veterinary APIs.

Here’s the breakdown:

| Category | Lab Testing Stage | Pilot Stage | Commercialized | Total |

|---|---|---|---|---|

| Pharma Intermediates | 37 | 18 | 22 | 77 |

| APIs | 12 | 10 | 18 | 40 |

| Nutraceutical APIs | – | – | 20 | 20 |

| Personal Care Intermediates | – | – | 3 | 3 |

| Veterinary API Products | – | – | 2 | 2 |

| Total Products | 49 | 28 | 65 | 142 |

This wide-ranging portfolio gives Anlon Healthcare a competitive edge, as it caters to multiple end-user industries and keeps expanding to match evolving pharmaceutical needs.

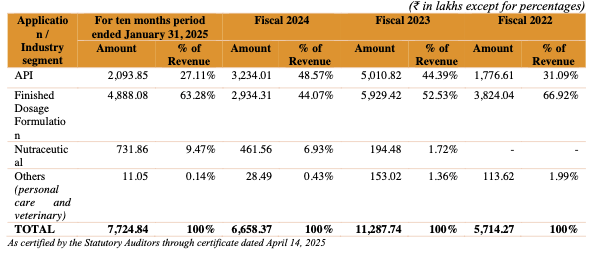

Revenue Mix and Market Reach

The company generates revenues from diverse applications, with Finished Dosage Formulations and APIs being the largest contributors.

For the ten months ended January 2025, revenue distribution stood at:

- APIs: ₹2,093.85 lakhs (27.11%)

- Finished Dosage Formulations: ₹4,888.08 lakhs (63.28%)

- Nutraceuticals: ₹731.86 lakhs (9.47%)

- Others (personal care and veterinary): ₹11.05 lakhs (0.14%)

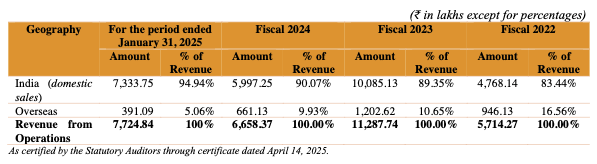

On the geographical front, Anlon Healthcare serves over 15 countries, including Italy, Germany, South Korea, China, Argentina, Mexico, Brazil, and the UK, besides a strong domestic market presence. Exports contributed 5.06% of revenue in FY2025 (10M), compared to 16.56% in FY2022, reflecting fluctuations but also a steady commitment to overseas expansion.

Scale of Operations

The company manufactured and sold 154 MT of APIs and Pharma Intermediates during the ten months ended January 2025, catering to 32 customers. In earlier years, customer counts were higher — 39 in FY2024, 48 in FY2023, and 63 in FY2022 — showing both market consolidation and a focus on key partnerships.

Anlon Healthcare IPO – Financial Performance

Anlon Healthcare has shown strong financial growth over the last three years, reflecting both business expansion and a sharper focus on profitability. While revenues have seen some fluctuations, profitability and net worth have strengthened significantly, positioning the company well for future scaling.

Financial Summary (₹ in Crore)

| Particulars | 31 Jan 2025 | FY24 | FY23 | FY22 |

|---|---|---|---|---|

| Assets | 160.96 | 128.00 | 111.55 | 84.97 |

| Total Income | 77.37 | 66.69 | 113.12 | 57.54 |

| Profit After Tax (PAT) | 11.96 | 9.66 | 5.82 | -0.11 |

| Net Worth | 71.86 | 21.03 | 7.37 | 1.55 |

| Reserves & Surplus | 32.01 | 5.03 | -4.63 | -10.24 |

| Total Borrowing | 62.39 | 74.56 | 66.39 | 60.32 |

Analysis:

- Revenue Trend: FY23 saw unusually high revenue (₹113.12 Cr), which dipped in FY24 but has picked up again in FY25 (₹77.37 Cr in 10M). This suggests volatility in sales but overall upward momentum.

- Profitability: From a loss of ₹0.11 Cr in FY22, the company has turned into a consistently profitable player, reporting ₹11.96 Cr PAT in 10M FY25.

- Balance Sheet Strength: Net worth has multiplied sharply from ₹1.55 Cr in FY22 to ₹71.86 Cr in FY25 (10M), showing strong value creation for shareholders.

- Debt Levels: Borrowings remain significant, but the company has started reducing them (₹62.39 Cr in FY25 vs ₹74.56 Cr in FY24).

Key Ratios (FY25)

| Ratio | Value |

|---|---|

| ROCE | 21.93% |

| Debt/Equity | 0.73 |

| RoNW | 25.21% |

| PAT Margin | 17.06% |

| EBITDA Margin | 26.88% |

Analysis:

- Return Ratios: A RoNW of 25.21% and ROCE of 21.93% reflect efficient use of capital and strong profitability relative to equity.

- Debt Situation: With a Debt/Equity of 0.73, leverage is moderate but trending lower, giving financial flexibility.

- Margins: EBITDA margin of 26.88% and PAT margin of 17.06% highlight operational efficiency and profitability in line with strong API/intermediates businesses.

💡 Takeaway:

Anlon Healthcare has transitioned from a small, loss-making company in FY22 to a high-margin, fast-growing player in the pharma intermediates and API space. While revenue fluctuations remain a risk, its strengthening balance sheet, healthy margins, and strong RoNW make the company’s fundamentals attractive for IPO investors.

Valuation & Peer Comparison

Valuation is one of the most critical factors for investors while considering any IPO. For Anlon Healthcare, the pre-IPO valuation indicates reasonable pricing compared to listed peers in the chemicals and pharma intermediates space.

Valuation Metrics (Pre-IPO)

| Metric | Value |

|---|---|

| EPS (₹) | 6.38 |

| P/E (x) | 14.26 |

| Price to Book (P/BV) | 4.51 |

| RoNW (%) | 25.21 |

Analysis:

- At a P/E of 14.26x, the IPO looks attractively priced compared to sector averages (most peers trade above 25x).

- P/BV of 4.51x also indicates fair pricing, considering the company’s RoNW of 25.21%.

- The valuation leaves enough room for listing gains as well as long-term appreciation, especially if the company maintains its profitability growth.

Peer Comparison

| Company Name | EPS (₹) | NAV (₹) | P/E (x) | RoNW (%) | P/BV Ratio |

|---|---|---|---|---|---|

| Anlon Healthcare Ltd. | 6.38 | 20.18 | 14.26 | 25.51 | 4.51 |

| Kronox Lab Sciences Ltd. | 6.91 | 24.28 | 26.18 | 28.26 | 7.50 |

| Acutaas Chemicals Ltd. | 19.81 | 161.24 | 58.47 | 12.15 | 7.19 |

| Supriya Lifescience Ltd. | 23.35 | 123.85 | 29.27 | 18.86 | 5.55 |

Analysis:

- Cheaper than peers on valuation: Anlon’s P/E (14.26x) is much lower than Kronox (26.18x), Supriya (29.27x), and Acutaas (58.47x).

- Efficient on return ratios: With RoNW of 25.51%, Anlon stands at par with Kronox (28.26%) and well above Acutaas (12.15%) and Supriya (18.86%).

- Price-to-Book value (4.51x) is lower than peers like Kronox (7.50x) and Acutaas (7.19x), which suggests a reasonable entry point for investors.

💡 Takeaway:

Anlon Healthcare’s IPO valuation appears undemanding and attractive compared to listed peers. The company combines high RoNW and margins with lower-than-sector P/E, making it a potentially compelling bet both for short-term listing gains and long-term investment.

Strengths & Risks Of Anlon Healthcare IPO

| Strengths | Risks / Concerns |

|---|---|

| Strong Financial Growth: Revenue and PAT have grown steadily, with PAT jumping to ₹11.96 Cr (31 Jan 2025) vs. ₹-0.11 Cr in FY22. | Dependence on Key Products: A large portion of revenue is dependent on a limited product portfolio, exposing it to demand fluctuations. |

| Healthy Margins: EBITDA margin at 26.88% and PAT margin at 17.06% indicates operational efficiency. | High Borrowings: Despite improvement, debt remains significant (₹62.39 Cr as of Jan 2025), keeping debt-equity ratio at 0.73. |

| Strong Return Ratios: RoNW at 25.21% and ROCE at 21.93% reflects efficient use of capital. | Volatility in Raw Material Prices: Being in pharma-chemical space, margins can be impacted by fluctuations in input costs. |

| Attractive Valuation vs Peers: P/E of 14.26x is far lower than industry average, leaving scope for rerating. | Competitive Industry: Operates in a fragmented and highly competitive industry, where established players like Supriya Lifescience and Kronox may hold stronger market positions. |

| Improving Balance Sheet: Rising net worth (₹71.86 Cr in Jan 2025 vs. ₹1.55 Cr in FY22) and reserves growth shows strengthening fundamentals. | Regulatory Risks: Pharma/chemical industry is subject to strict global and domestic compliance, which can affect operations if regulations change. |

💡 Balanced View:

Anlon Healthcare has shown remarkable financial turnaround, backed by strong profitability, high returns, and attractive valuations. However, debt levels, competitive pressures, and regulatory risks remain areas to watch.

Anlon Healthcare IPO GMP (Grey Market Premium)

The Grey Market Premium (GMP) is often tracked by investors to gauge listing expectations. For Anlon Healthcare IPO, the GMP has remained flat at ₹0 as of 21 August 2025.

GMP Trend

| Date | IPO Price | GMP | Estimated Listing Price | Estimated Profit / Loss |

|---|---|---|---|---|

| 21 Aug 2025 | ₹91 | ₹0 | ₹91 (0.00%) | ₹0 |

Analysis:

- Currently, there is no premium in the grey market, which suggests that investors are adopting a wait-and-watch approach.

- Factors like company fundamentals, valuations (P/E 14.26x, P/BV 4.51x), and market sentiment will play a more decisive role in listing performance than grey market signals.

- Often, IPOs with solid financials and attractive valuations (like Anlon Healthcare) can still surprise on listing day, even if GMP is muted.

Conclusion – View on Anlon Healthcare IPO

The Anlon Healthcare IPO presents a mixed picture for investors. On one hand, the company has shown strong financial performance with rising profits, robust margins (EBITDA margin 26.88%, PAT margin 17.06%), and a healthy RoNW of 25.21%. Its balance sheet also reflects improving net worth and reduced leverage compared to previous years.

On the other hand, the muted GMP of ₹0 indicates that the market sentiment is cautious. This could be due to recent IPO saturation, sector dynamics, or investors waiting for clearer signals before committing.

From a valuation perspective, Anlon is reasonably priced at P/E of 14.26x compared to peers like Kronox Lab (26.18x) and Supriya Lifescience (29.27x). Its P/BV of 4.51 is also lower than some peers, suggesting that the IPO is not aggressively priced.

Overall, Anlon Healthcare offers value for long-term investors with its improving fundamentals, while short-term listing gains may remain uncertain due to the flat GMP trend.

Short-Term Strategy

- Given the current ₹0 GMP, immediate listing gains look limited.

- Investors seeking short-term profit should be cautious and may prefer to wait for market sentiment closer to listing day.

Long-Term Strategy

- Anlon Healthcare has demonstrated consistent revenue growth and strong return ratios.

- With improving financial health and a scalable business model, it holds promise for long-term wealth creation.

- Long-term investors with moderate risk appetite may consider subscribing.

Allotment Strategy

- With cautious grey market signals, HNI oversubscription may stay moderate.

- Retail investors applying 1–2 lots may still stand a fair chance of allotment.

- Serious long-term investors can consider applying in full retail quota for better chances.

Final Takeaway:

“Anlon Healthcare IPO might not sparkle in the grey market, but its fundamentals shine for investors who believe in long-term value over short-term hype.”

FAQs on Anlon Healthcare IPO:

1. What is the Anlon Healthcare IPO?

The Anlon Healthcare IPO is a mainboard public issue aiming to raise funds for expansion, working capital, and general corporate purposes.

2. What is the IPO price band of Anlon Healthcare?

The IPO price is fixed at ₹91 per share.

3. What is the lot size for Anlon Healthcare IPO?

Investors can bid for a minimum of 1 lot (160 shares) and in multiples thereafter.

4. What is the Anlon Healthcare IPO issue size?

The IPO size is ₹91.20 crore (approximate).

5. When will the Anlon Healthcare IPO open and close?

The IPO is expected to open on 26 August 2025 and close on 28 August 2025 (tentative).

6. What is the Anlon Healthcare IPO market capitalization?

Post issue, the company’s market capitalization is estimated at ₹483.68 crore.

7. What are Anlon Healthcare’s key financial highlights?

The company reported a PAT of ₹11.96 crore (FY25 Jan-end) with strong margins and improving net worth.

8. What is the Anlon Healthcare IPO GMP today?

As of 21 August 2025, the GMP is ₹0, suggesting no listing premium.

9. Should I apply for Anlon Healthcare IPO for listing gains?

Short-term listing gains appear uncertain due to the flat GMP trend.

10. Is Anlon Healthcare IPO good for long-term investment?

Yes, due to strong financial performance, scalable business model, and reasonable valuation, it looks favorable for long-term investors.

Related Articles

How to Analyze an IPO Before Investing: A Step-by-Step Guide

One Demat vs Multiple Demat – Which is Better for IPO Allotment?