Amanta Healthcare IPO – A Closer Look

The Amanta Healthcare IPO is all set to open for subscription on 1st September 2025, bringing investors an opportunity to participate in one of India’s leading sterile solutions and IV fluids manufacturers. With a strong presence in parenteral drugs, IV fluids, ophthalmic products, and contract manufacturing, Amanta has carved out a niche in the critical healthcare segment.

The company plans to raise up to ₹126 crore through a fresh issue of 1 crore equity shares, with a price band expected between ₹120 – ₹126 per share. The proceeds will largely be used for capacity expansion, debt repayment, and working capital needs, signaling a push for future growth.

Given its over 25 years of experience, international certifications, and an export footprint spanning more than 15 countries, the Amanta Healthcare IPO has caught the attention of both retail and institutional investors. But does its financial performance and valuation justify a strong listing? Let’s break it down section by section.

Amanta Healthcare IPO Details

A fresh issue mainboard offering aimed at scaling sterile manufacturing capacity and strengthening operations.

IPO Snapshot

| Particulars | Details |

|---|---|

| Issue Type | Bookbuilding (Mainboard) |

| Sale Type | Fresh issue only |

| Issue Size | ₹126.00 Cr (1,00,00,000 shares) |

| Price Band | ₹120 – ₹126 per share |

| Face Value | ₹10 per share |

| Lot Size | 119 shares |

| Minimum Retail Investment | ₹14,280 (at ₹120) / ₹14,994 (at ₹126) |

| Listing | BSE, NSE |

| Pre-Issue Shares | 2,88,29,351 |

| Post-Issue Shares | 3,88,29,351 |

| BRLM | Beeline Capital Advisors Pvt. Ltd. |

| Registrar | MUFG Intime India Pvt. Ltd. |

Important Dates (Tentative)

| Event | Date |

|---|---|

| IPO Opens | Mon, Sep 1, 2025 |

| IPO Closes | Wed, Sep 3, 2025 |

| Allotment Finalization | Thu, Sep 4, 2025 |

| Refunds Initiation | Fri, Sep 5, 2025 |

| Shares Credit to Demat | Fri, Sep 5, 2025 |

| Listing Date | Mon, Sep 8, 2025 |

| UPI Mandate Cut-off | 5 PM, Sep 3, 2025 |

Objects of the Issue

- ₹70.00 Cr – Capex for civil works, equipment, plant & machinery to set up a new SteriPort manufacturing line at Hariyala, Kheda (Gujarat).

- ₹30.13 Cr – Capex for civil works, equipment, plant & machinery to set up a new SVP manufacturing line at Hariyala, Kheda (Gujarat).

- General corporate purposes.

Company Overview & Business Model – Amanta Healthcare Ltd.

Amanta Healthcare Ltd. is a pharmaceutical company specializing in the development, manufacturing, and marketing of sterile liquid parenteral products. The company leverages advanced technologies such as Aseptic Blow-Fill-Seal (ABFS) and Injection Stretch Blow Moulding (ISBM) to produce both Large Volume Parenterals (LVPs) and Small Volume Parenterals (SVPs). Its product portfolio spans six key therapeutic segments – fluid therapy (IV fluids), formulations, diluents & injectables, ophthalmic, respiratory care, and irrigation solutions.

In addition to parenterals, Amanta also manufactures a range of medical devices including irrigation solutions, first-aid products, and eye lubricants. With container volumes ranging from 2 ml to 1000 ml and multiple closure systems like nipple head, twist-off, leur-lock, and screw types, the company caters to diverse medical needs.

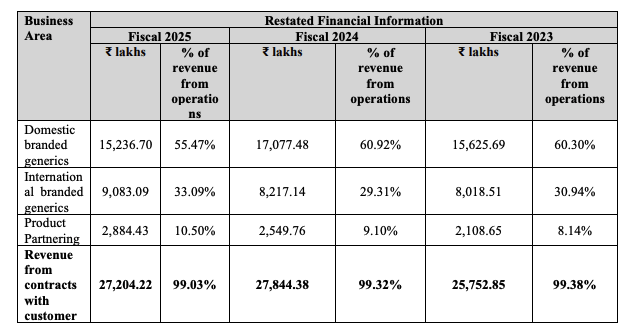

Business Segments

Amanta operates through three strategic business units:

- Domestic Branded Generics – Products marketed under its own brands through a vast distribution network of over 320 distributors and stockists across India. This segment contributed 55.47% of revenues in FY25.

- International Branded Generics – Exports to emerging and semi-regulated markets such as Africa, Latin America, and the UK. As of FY25, the company’s products were registered across 120 international jurisdictions and exported to 21 countries, contributing 33.09% of revenues.

- Product Partnering – Large-scale contract manufacturing and loan licensing for other pharmaceutical companies. This segment generated 10.50% of revenues in FY25.

Manufacturing & R&D Capabilities

The company operates a state-of-the-art manufacturing facility in Hariyala, Gujarat, equipped with four LVP lines (two ABFS and two ISBM) and three SVP lines (two ABFS and one conventional line). The facility holds WHO-GMP certifications and approvals from multiple international regulatory bodies including Cambodia, Sudan, Zimbabwe, and the Philippines.

Amanta also has a dedicated Formulation & Development (F&D) and quality control laboratory, enabling it to innovate, improve formulations, and develop products for both domestic and global markets. Its cGMP-certified operations allow production of a wide range of sterile liquid formulations, including quinolones, antibiotics, antifungals, diuretics, ophthalmic, and respiratory products.

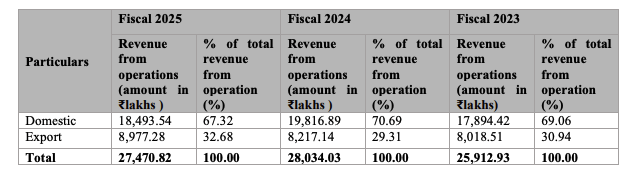

Revenue Mix

For FY25, Amanta Healthcare reported revenues of ₹27,470.82 lakhs, with:

- 67.32% from domestic markets

- 32.68% from exports

This balanced revenue mix demonstrates the company’s strong domestic presence along with growing international reach.

Management & Workforce

Led by Bhavesh Patel, Managing Director and Promoter, Amanta is backed by a professional team of over 123 employees in R&D and quality control, and 96 sales and marketing personnel in its domestic branded generics division. The company emphasizes strong distributor relationships, attractive packaging, and incentive-driven schemes as growth drivers.

Financial Highlights – Amanta Healthcare Ltd.

Amanta Healthcare Ltd. has demonstrated a steady improvement in profitability despite a marginal dip in revenues in FY25. The company’s focus on operational efficiency and debt reduction has resulted in stronger margins and healthier bottom-line growth.

Financial Performance (₹ in Crores)

| Particulars | FY25 | FY24 | FY23 | Trend |

|---|---|---|---|---|

| Total Income | 276.09 | 281.61 | 262.70 | ⬇️ -2% YoY |

| Revenue from Operations | 274.71 | 280.34 | 259.13 | Slight dip in FY25 |

| EBITDA | 61.05 | 58.76 | 56.31 | Stable margin expansion |

| EBITDA Margin | 22.11% | 20.86% | 21.43% | Improved efficiency |

| Profit After Tax (PAT) | 10.50 | 3.63 | -2.11 | Strong turnaround |

| PAT Margin | 3.86% | 1.30% | -0.82% | Significant improvement |

| Net Worth | 96.39 | 66.29 | 62.88 | Strengthened capital |

| Reserves & Surplus | 67.56 | 39.46 | 36.05 | Rising steadily |

| Total Borrowings | 195.00 | 205.23 | 215.66 | Gradual reduction |

(Source: RHP, Restated Consolidated Financials)

Key Takeaways

- Revenue: Marginal decline of 2% YoY in FY25 to ₹276.09 Cr, after witnessing 8.2% growth in FY24.

- Profitability: PAT surged 189% YoY in FY25 to ₹10.50 Cr, highlighting operational efficiency.

- Margins: EBITDA margin improved to 22.11% in FY25, indicating stronger cost control.

- Balance Sheet: Net worth expanded to ₹96.39 Cr, while borrowings reduced from ₹215.66 Cr in FY23 to ₹195 Cr in FY25.

- Cash Flow: Net cash flow from operating activities stood at ₹46.62 Cr in FY25, reflecting robust internal cash generation.

Key Ratios & KPIs (FY25)

- Return on Equity (ROE): 12.42%

- Return on Capital Employed (ROCE): 13.72%

- Return on Net Worth (RoNW): 10.89%

- PAT Margin: 3.86%

- EBITDA Margin: 22.11%

- Debt-to-Equity Ratio: 2.02 (improved from 3.10 in FY24)

- Market Capitalization (Post IPO): ₹489.25 Cr

Financial Overview

Amanta Healthcare’s financials highlight a company in turnaround mode – while revenues remain stable, profitability and margins have shown sharp improvements. Reduction in debt levels and strong operating cash flows further strengthen its financial resilience.

Valuation and Peer Comparison – Amanta Healthcare IPO

The valuation of Amanta Healthcare IPO suggests that the company is entering the market at a relatively premium pricing, considering its earnings base and return ratios.

Valuation Snapshot

| Particulars | Pre-IPO | Post-IPO |

|---|---|---|

| EPS (₹) | 3.64 | 2.70 |

| P/E (x) | 34.59 | 46.59 |

| Price to Book Value (P/BV) | — | 3.77 |

- Based on the FY25 EPS of ₹2.70 (Post-IPO), the company is demanding a P/E multiple of ~46.6x at the upper price band.

- The P/BV ratio stands at 3.77x, which indicates higher valuations compared to some peers.

Peer Comparison (As per RHP)

| Company | EPS (₹) | NAV (₹) | P/E (x) | RoNW (%) | P/BV (x) |

|---|---|---|---|---|---|

| Amanta Healthcare Ltd. | 3.71 | 33.43 | 33.92 | 10.89 | 3.82 |

| Denis Chem Lab Ltd. | 5.82 | 61.33 | 15.92 | 9.49 | 1.51 |

(Source: RHP, as on March 31, 2025)

- Compared to Denis Chem Lab Ltd., Amanta Healthcare is valued at a much higher P/E and P/BV, though its RoNW is slightly better.

- This indicates that investors are paying a valuation premium for Amanta’s growth potential and improved financial performance.

📌 Note: The RHP also mentions a few other peer companies in the pharmaceutical formulations and healthcare manufacturing space. However, since these peers are unlisted, they are not directly comparable with Amanta Healthcare’s listed valuation metrics.

Valuation Overview

While Amanta Healthcare has showcased improved profitability and stronger margins, the IPO is priced at a higher earnings multiple compared to listed peers. This premium could be justified if the company sustains its earnings growth trajectory, continues deleveraging, and leverages the upcoming IPO funds for capacity expansion and working capital.

Strengths and Risks – Amanta Healthcare IPO

| Strengths | Risks |

|---|---|

| Diversified product portfolio – Company manufactures sterile liquid parenterals (ampoules, vials, BFS) used in hospitals and healthcare, catering to both domestic and export markets. | High debt levels – Debt/Equity ratio of 2.02 (FY25) shows financial leverage remains high, though reducing vs. previous years. |

| Strong turnaround in profitability – PAT jumped 189% YoY in FY25 to ₹10.5 Cr, supported by improved operational efficiency. | Premium valuation – At ~46.6x P/E (post-IPO), the stock is priced higher than listed peers, leaving limited margin of safety. |

| Robust EBITDA margins – Consistent 20–22% EBITDA margin over the last three years, highlighting operational efficiency. | Dependency on few large customers – Any change in orders or terms can significantly impact revenues. |

| Growing demand for sterile formulations – Rising domestic healthcare demand and export opportunities in Africa, Asia, and Latin America. | Regulatory & compliance risk – Business depends heavily on regulatory approvals (WHO-GMP, USFDA, etc.), and non-compliance can impact operations. |

| Improving return ratios – RoE improved to 12.4% in FY25 vs. 5.3% in FY24, reflecting better utilization of equity capital. | Revenue stagnation – FY25 revenue fell 2% YoY, showing topline growth challenges despite profit recovery. |

| Experienced promoters & established track record – Over 25 years of presence in the pharma manufacturing industry. | Foreign exchange fluctuations – Export exposure makes earnings sensitive to currency movements. |

Amanta Healthcare IPO GMP (Grey Market Premium)

The Grey Market Premium (GMP) gives investors an early signal of listing expectations. As of the latest update, the Amanta Healthcare IPO is witnessing healthy interest in the unofficial market.

Amanta Healthcare IPO GMP Trend

| GMP Date | IPO Price (₹) | GMP (₹) | Sub2 Sauda Rate | Estimated Listing Price (₹) | Estimated Profit* |

|---|---|---|---|---|---|

| 28-08-2025 | 126.00 | ₹22 (Up) | 2000/28000 | ₹148 (17.46%) | ₹2618 |

Note: GMP is subject to market sentiments and may vary till the listing date. Investors should not solely rely on GMP for investment decisions.

Conclusion – View on Amanta Healthcare IPO

The Amanta Healthcare IPO offers investors exposure to a well-established pharmaceutical company with a presence in IV fluids and other healthcare products. Backed by improving profitability (PAT up 189% YoY in FY25), healthy EBITDA margins (22.11%), and reduction in debt-equity ratio, the company is showcasing operational improvements. However, its high leverage, moderate return ratios, and valuation premium compared to peers need careful consideration.

Short-Term View (Listing Gains)

With a positive GMP of ₹15, the IPO is expected to list at around an 11–12% premium over the issue price of ₹126. Given strong subscription demand and improving fundamentals, short-term investors may benefit from listing gains.

Long-Term View

For long-term investors, Amanta Healthcare’s focus on healthcare infrastructure, steady margins, and scope for debt reduction provide potential. But considering its higher P/E multiple (46.59 post-IPO) compared to listed peer Denis Chem Lab (15.92 P/E), the stock looks expensive. Hence, long-term investors should weigh valuation risks before committing.

Allotment Strategy

- Aggressive / short-term investors may apply for listing gains, supported by GMP trends.

- Conservative / long-term investors should evaluate post-listing price movements and business scaling before making large commitments.

- Retail applicants may consider one lot application to test listing momentum.

Amanta Healthcare IPO brings listing gain potential, but long-term investors must weigh high valuations against improving fundamentals before making their move.

FAQs on Amanta Healthcare IPO

1. What is the Amanta Healthcare IPO opening and closing date?

The IPO opens on September 1, 2025 and closes on September 3, 2025.

2. What is the IPO price band of Amanta Healthcare?

The price band is fixed at ₹120 – ₹126 per share.

3. What is the lot size for Amanta Healthcare IPO?

The lot size is 118 shares, and retail investors can apply for a maximum of 13 lots.

4. What is the issue size of Amanta Healthcare IPO?

The total issue size is 1 crore equity shares, aggregating up to ₹120 – ₹126 crore.

5. What type of issue is Amanta Healthcare IPO?

It is a 100% fresh issue of equity shares.

6. What is the minimum investment required?

Retail investors need a minimum of ₹14,868 (at ₹126 per share) to apply.

7. On which exchange will Amanta Healthcare shares be listed?

The shares will be listed on both NSE and BSE (Mainboard IPO).

8. Who are the lead managers of the IPO?

The book-running lead managers are Choice Capital Advisors Pvt Ltd.

9. What is the GMP (Grey Market Premium) of Amanta Healthcare IPO?

As of August 25, 2025, the GMP is around ₹15, indicating a listing price near ₹141.

10. Is Amanta Healthcare IPO good for long-term investment?

It offers strong fundamentals and growth prospects, but the high valuation and debt levels require cautious long-term evaluation.

Related Articles

How to Analyze an IPO Before Investing: A Step-by-Step Guide

One Demat vs Multiple Demat – Which is Better for IPO Allotment?